🆕NEW: The Amortization Simulator now automatically updates Bank of Canada rate change dates when you change the closing date. Here's a 90-second video of how it works: link.

There hasn't been this much buzz before a U.S. policy easing cycle since 1981.

Virtually this entire

NEW: The Amortization Simulator now automatically updates Bank of Canada rate change dates when you change the closing date. Here's a 90-second video of how it works: link.

There hasn't been this much buzz before a U.S. policy easing cycle since 1981.

Virtually this entire year, economists have played the guessing game on when in 2024 the Fed would cut. That's led borrowers down a long road of anticipation.

Now, we're almost on the eve of it. And it's hard to overstate the significance of the Fed giving the all-clear sign for inflation—particularly the significance for Canadian mortgage rates.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

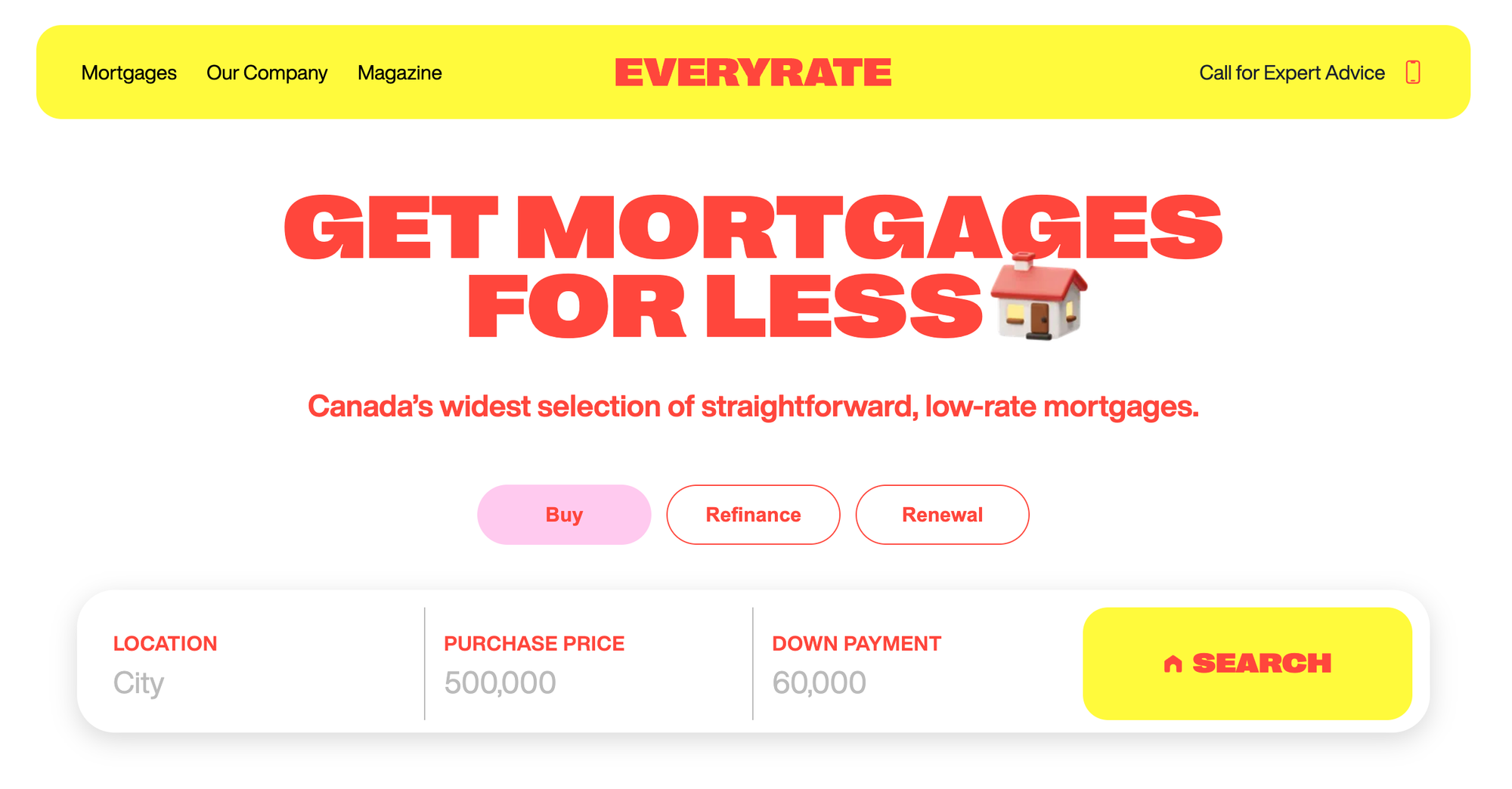

Canada has a shiny new rate comparison website. It's called EveryRate.ca.

If you're a broker or lender, you may be rolling your eyes, thinking, we need another rate comparison site like Jeff Bezos needs a penny.

But, for EveryRate.ca co-founder Andy Hill, it'

Canada has a shiny new rate comparison website. It's called EveryRate.ca.

If you're a broker or lender, you may be rolling your eyes, thinking, we need another rate comparison site like Jeff Bezos needs a penny.

But, for EveryRate.ca co-founder Andy Hill, it's simply about serving up what consumers hunger for: juicier deals.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Analysts have been chatting up a storm about how all the extra cash folks saved up is like a financial superhero cape for homeowners. Yet, a new CIBC report suggests that household savings won't be enough to save the mortgage renewers who need the most help.

Turns out,

Analysts have been chatting up a storm about how all the extra cash folks saved up is like a financial superhero cape for homeowners. Yet, a new CIBC report suggests that household savings won't be enough to save the mortgage renewers who need the most help.

Turns out, that middle-income crowd—those with mortgages—aren't exactly the saving champs you'd hope. The bank's research finds they actually have low liquidity and are vulnerable.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Rates have jumped several hurdles in the last few weeks, from CPI to GDP to job numbers. Bond yields have powered through it all to close on Friday at a 17-month low.

There's not much on the radar this week that should foreseeably force yields back up. Canada&

Rates have jumped several hurdles in the last few weeks, from CPI to GDP to job numbers. Bond yields have powered through it all to close on Friday at a 17-month low.

There's not much on the radar this week that should foreseeably force yields back up. Canada's economic calendar is light until September 17, and U.S. CPI inflation (the week's highlight) is expected to land near consensus at 2.6% y/y.

Post this quiet spell, expect the plot to thicken.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

If you're a mortgage originator and none of your CRM emails include graphs, it's time to jazz them up. Visuals tell stories better than words. Charts, in particular, accelerate comprehension and turn newsletters into less blah, more ah-ha.

That's why mortgage clients and referral

If you're a mortgage originator and none of your CRM emails include graphs, it's time to jazz them up. Visuals tell stories better than words. Charts, in particular, accelerate comprehension and turn newsletters into less blah, more ah-ha.

That's why mortgage clients and referral sources rarely grumble when you hit them with a relevant chart. ("Relevant," meaning it tells a compelling story that potentially impacts their net worth.)

That's also why we're thrilled to announce the updated AI Copilot for MLN Pro members. This revised chart builder is now easily accessible from anywhere in the Mortgage Command Centre (MCC).

Chart Copilot 2.0 makes it faster to build custom graphs thanks to:

Improved logic (i.e., the AI recognizes and follows instructions better)

A more straightforward interface (just click the floating button in the lower right corner).

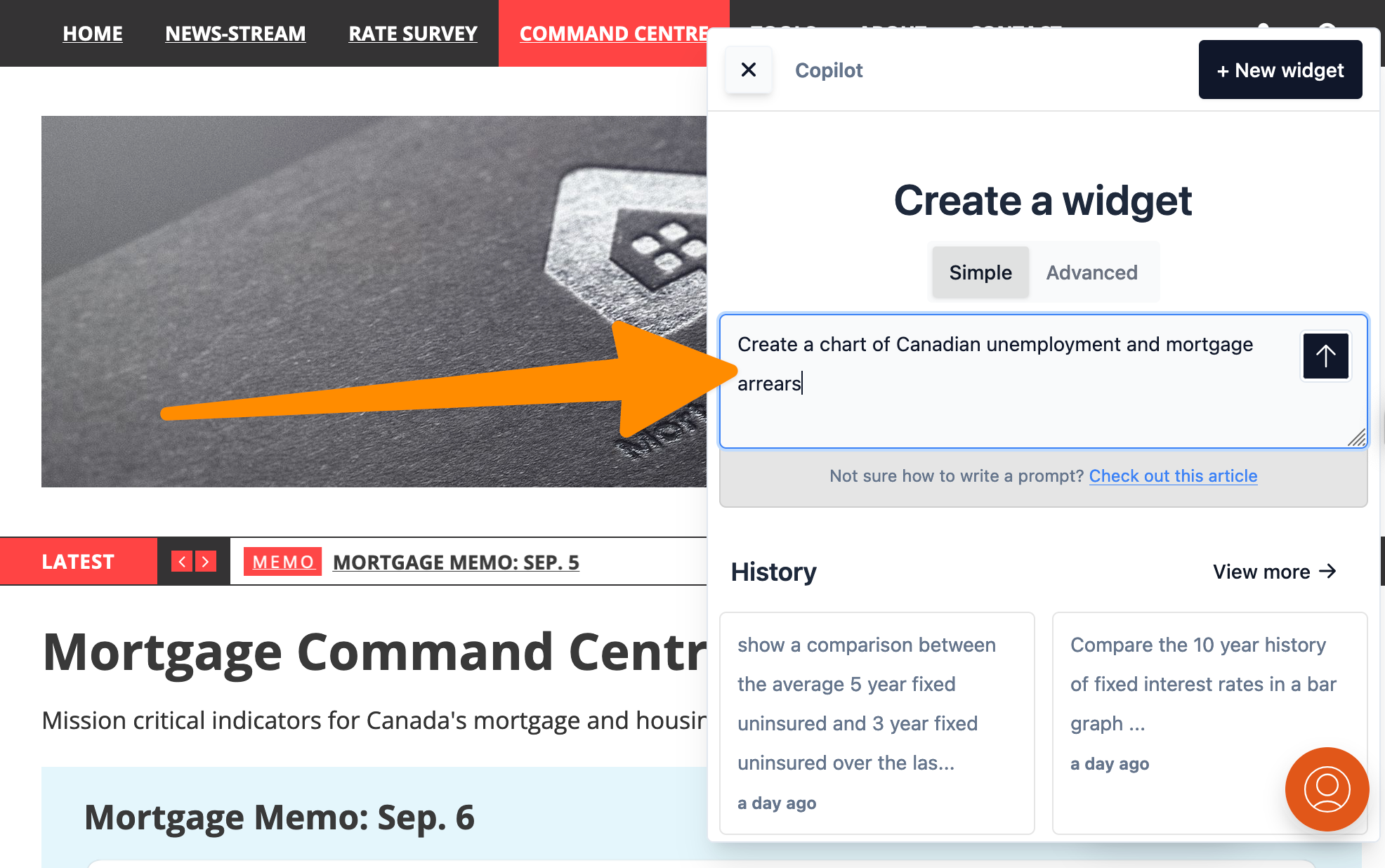

Along with smarter AI, the best part is that you can now see what you're doing in a pop-up "Copilot" window. No more typing a prompt and then having to scroll way up the screen like your finger's on a treadmill.

To make a chart

Click the <Chat with your data> button in the MCC

Tell it what you want to chart (here's all the available data)

For example, you could type: "Create a chart of Canadian unemployment and mortgage arrears."

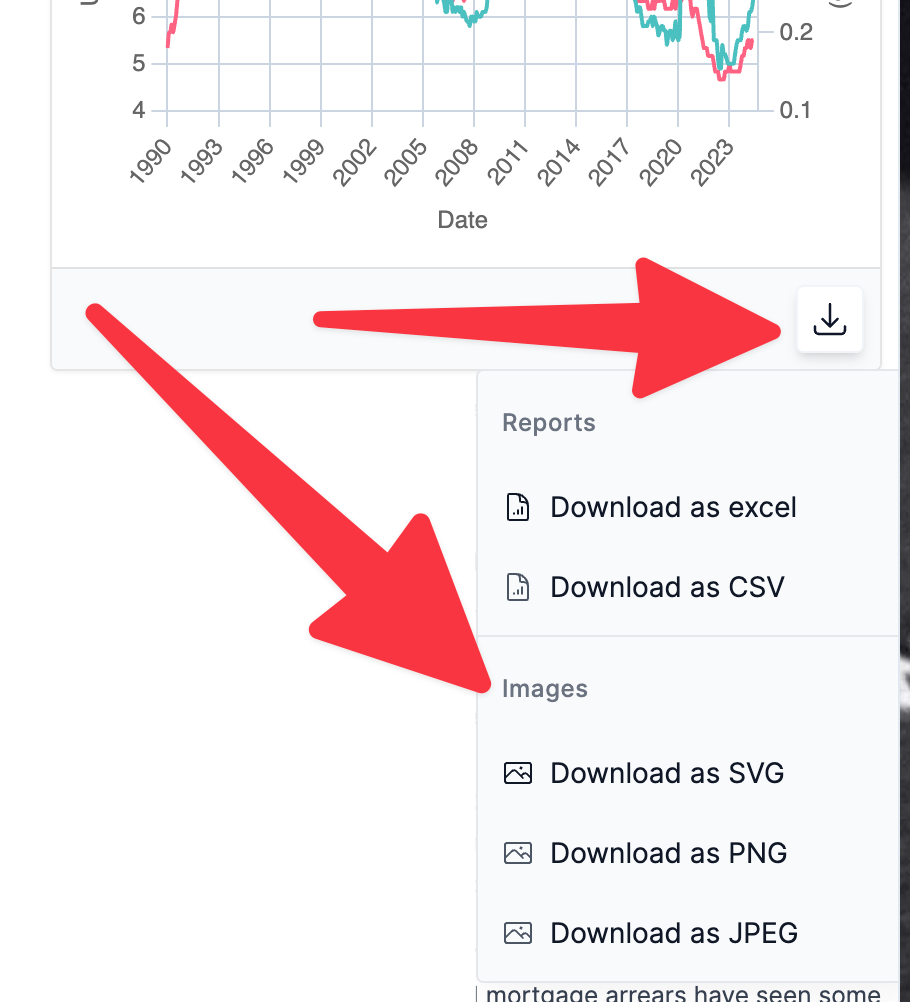

Make your chart pretty (change colours, line thickness, the title, the subtitle, etc.)

Download the chart or chart data (see below)

To change the chart colour to red, for example, type: "Change the line colour to red"

To eliminate points on chart lines, type: "Remove points on the chart lines"

To make chart lines thicker, type: "Increase line thickness by 1 point"

If you see a chart with blank space [like this], type: "Start the chart at January 1990" (pick a date where you see chart data start)

To hide the legend, type: "Hide the legend"

To change the title, type: "Change the title to "X" (pick whatever you want)

If you have any questions, email support anytime at info @ mortgagelogic . news. Meanwhile, plot it like it’s hot.

Mortgage Bytes

💡

Reader note: MLN's software provider for comments (Cove) has fixed a technical issue that prevented us from responding to your comments within our normal 24-hour goal.

Macklem hints at home price bump: Don't be surprised to see "some pickup in housing prices" as rates drop, Governor Macklem said last week. But higher home prices don't necessarily mean higher overall shelter inflation—not if we get lower rates, immigration and rents, he says. (Here's his response to MLN's question about it.)

Ourboro update: Shared equity investor, Ourboro, says it anticipates removing its waitlist "this fall." The company, which takes an equity stake in people's homes in exchange for down payment funds, has seen "overwhelming" demand. Chief Product Officer Alex Kjorven told MLN last week that there's no waitlist for homebuyers with 10% down, however (Ourboro contributes the other 10% in exchange for half the appreciation). She says that once the company's pilot with an undisclosed major bank is over, the company expects to have ample capital to meet demand. "We have phenomenon institutional backing," she says, including Fengate Asset Management.

📙"Budget 2024 announces the government’s intention to consult with the mortgage industry on making available a tool through the Canada Revenue Agency to complement the existing strategies of financial institutions to verify borrower income for mortgages."

—Page 88 of Budget 2024

Mortgage lenders and originators have been

"Budget 2024 announces the government’s intention to consult with the mortgage industry on making available a tool through the Canada Revenue Agency to complement the existing strategies of financial institutions to verify borrower income for mortgages."

Mortgage lenders and originators have been waiting for CRA digital income verification since dinosaurs roamed the earth. Or at least it feels that way.

How the government has waited this long to implement such a common-sense lending and anti-fraud improvement is mind-boggling. Seriously, Moses had an easier time getting those tablets.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.