You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

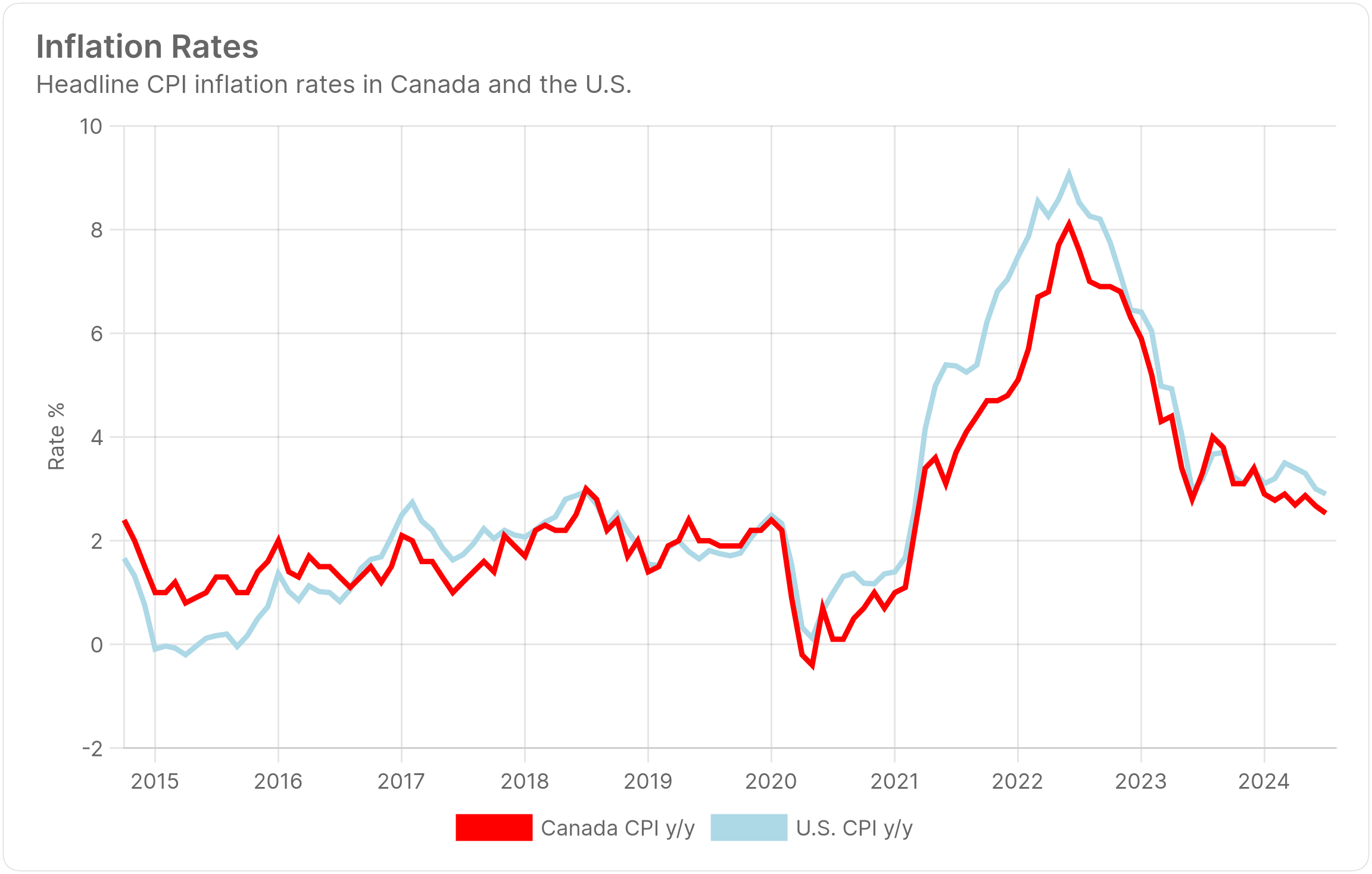

Canada's monetary barbers have trimmed another 25 bps off the top.

The Bank of Canada lowered its overnight rate to 4.25% today, sending four key messages in the process:

1. "We need to increasingly guard against the risk that the economy is too weak and inflation

Canada's monetary barbers have trimmed another 25 bps off the top.

The Bank of Canada lowered its overnight rate to 4.25% today, sending four key messages in the process:

"We need to increasingly guard against the risk that the economy is too weak and inflation falls too much."

"There is little evidence of broad-based price pressures."

"The slack in the labour market is expected to slow wage growth."

"Shelter price inflation is still too high. It remains the biggest contributor to overall inflation."

Apart from point 4, it's mostly good tidings for borrowers. Odds are, by this time next year, Ottawa's financial stylists will have given our rate market a whole new look.

Cash flow improves

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

With the inflation roller coaster of 2021-'23 and its savage rate hike cycle still fresh in our memories, millions of Canadians dread the thought of re-inflation.

They worry that the BoC will yell "Psych!" — and that rate cuts will boomerang back as hikes, punishing them for

With the inflation roller coaster of 2021-'23 and its savage rate hike cycle still fresh in our memories, millions of Canadians dread the thought of re-inflation.

They worry that the BoC will yell "Psych!" — and that rate cuts will boomerang back as hikes, punishing them for choosing a variable mortgage. For families on the budgetary edge, that broken promise of cuts would feel kind of like being sucker-punched by a loan shark.

Fortunately, that doesn't seem too likely at this point. The Bank of Canada, in its public messaging, is clearly more worried about disinflation than the opposite.

The country is suffering from "excess supply," says Governor Tiff Macklem. He's concerned about inflation falling too much, too fast, as that could coincide with more backbreaking job losses.

To prevent that, the Bank is inclined to keep trimming rates.

As for how aggressive it will be and for how long, even the BoC's crystal ball is cloudy on those points.

It's all riding on if—or how quickly—our economy turns into a dumpster fire. Aside from high inflation, the last thing the Bank of Canada wants is to keep monetary policy too tight and run into negative growth.

But how do you measure the risk of face-planting into a recession?

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

If you depend on a reverse mortgage for cash flow or sell them for a living, Steve Ranson has made your life better. In his quarter-century heading up Canada's first and biggest reverse mortgage company, the team he led made the product significantly less expensive, more feature-rich, less

If you depend on a reverse mortgage for cash flow or sell them for a living, Steve Ranson has made your life better. In his quarter-century heading up Canada's first and biggest reverse mortgage company, the team he led made the product significantly less expensive, more feature-rich, less stigmatized and more widely available.

During Ranson's extraordinary tenure, Canada's reverse mortgage market grew 100x. That's not just moving the needle; that's almost breaking the gauge.

Steve Ranson, Former CEO, HomeEquity Bank

In this exclusive interview, Ranson shares insights on:

The biggest development in Canada's reverse market over the last five years

The greatest challenge for reverse mortgages in the next five years

Three reasons why reverse mortgage rates are higher than regular rates

The impact of reverse mortgages on inheritances

Why big banks don't sell reverse mortgages directly (yet)

Why the company had to become a bank

How becoming a bank helped customers

Whether the spread between reverse and regular mortgages will narrow

How OSFI policy keeps rates higher

HomeEquity Bank's #1 goal (at the time he left)

How reverse mortgages are being used to help home buyers

Why the idea of downsizing has "gone away" in many markets

How seniors can use reverse mortgages in a retirement planning capacity

What percentage of borrowers don't pay off their reverse mortgage before they die

Why HomeEquity Bank doesn't have a HELOC reverse mortgage (hint: big banks are a factor)

The remarkable consistency of the average customer's age

Whether we'll approach a U.S.-style reverse mortgage adoption rate

The importance of securitization in the American reverse market

The impact of FHA on reverse mortgages in the U.S.

His two biggest regrets in the business

What he's most proud of in his 27 years at HomeEquity Bank.

That's a lot to pack into a 30-minute interview. Check out MLN's full discussion with Ranson below...

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

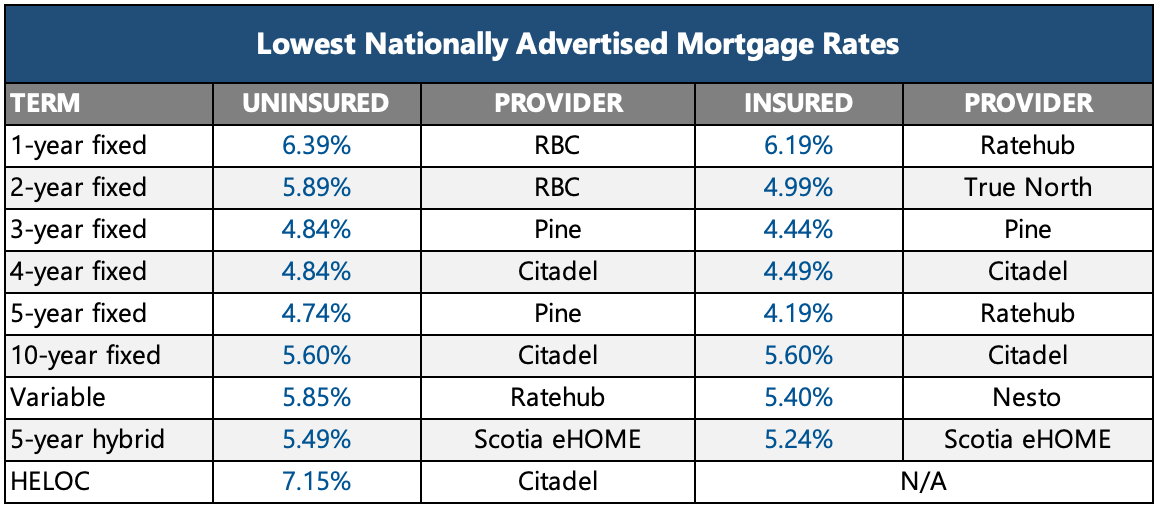

The last time 5-year fixed rates were this close to 4%, ChatGPT wasn't even a thing. And here we are, with the insured variety now as cheap as 4.19%.

With a decent U.S. PCE inflation report on Friday and #dovish# jobs data next week, 3.99%

The last time 5-year fixed rates were this close to 4%, ChatGPT wasn't even a thing. And here we are, with the insured variety now as cheap as 4.19%.

With a decent U.S. PCE inflation report on Friday and #dovish# jobs data next week, 3.99% insured rates could be winking at us as soon as next month.

Source: MLN Canadian Mortgage Rate Survey

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.