The BoC left its target rate anchored at 5% this morning, but hold the phone—it just got upstaged — by U.S. inflation.

America's reaccelerating CPI data stole the show this morning, sending bond traders into a bearish frenzy.

The BoC left the beacon on for 2024 rate

The BoC left its target rate anchored at 5% this morning, but hold the phone—it just got upstaged — by U.S. inflation.

America's reaccelerating CPI data stole the show this morning, sending bond traders into a bearish frenzy.

The BoC left the beacon on for 2024 rate cuts, however, despite keeping its lips zipped on the U.S. inflation letdown. Here's what mortgage hunters need to know in case the rate waters get rough.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

It feels counterintuitive, but simple arithmetic shows the #BoC#'s 2% promised land is within reach.

That's partly why the Bay Street brain trust is amping up calls for the first rate cut in June. Economists' resurgent confidence follows Canadian joblessness topping 6% and y/y

It feels counterintuitive, but simple arithmetic shows the #BoC#'s 2% promised land is within reach.

That's partly why the Bay Street brain trust is amping up calls for the first rate cut in June. Economists' resurgent confidence follows Canadian joblessness topping 6% and y/y CPI undershooting 3%.

But here's the main reason a summer rate cut isn't just pie in the sky.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

📰Also in this edition:

• Canadian / U.S. rates to diverge

• Mortgage Bytes

So, here's a 'coincidence.' The day after we run a story on potential mortgage changes, JT plays coy when reporters ask him about 30-year insured amortizations:

“On mortgages, we will have more to say

Also in this edition: • Canadian / U.S. rates to diverge • Mortgage Bytes

So, here's a 'coincidence.' The day after we run a story on potential mortgage changes, JT plays coy when reporters ask him about 30-year insured amortizations:

“On mortgages, we will have more to say between now and the budget date on April 16, and perhaps we will save it for April 16.”—Justin Trudeau at a news conference Friday

Trudeau's poker face has a tell. And with any luck, he might have an ace up his sleeve: a pro-mortgage-growth ace.

The money's on 30-year amortizations

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

With votes on the line and its survival hanging in the balance, the Liberal government needs to start pulling rabbits out of hats.

And it doesn't take a Mensa member to figure out who the Liberals must win over. It's the young and restless twenty- and

With votes on the line and its survival hanging in the balance, the Liberal government needs to start pulling rabbits out of hats.

And it doesn't take a Mensa member to figure out who the Liberals must win over. It's the young and restless twenty- and thirty-somethings—the people who've swapped their Liberal loyalty cards for a shot at affording a home where their roommate's name isn't Mom.

The latest Nanos poll is a horror show for the Libs. Older Gen-Zs and younger Millenials have deserted Team Trudeau in droves, with only 14% of Canadians aged 30 to 39 supporting this government. This political catastrophe is due mainly to unaffordable housing and living expenses, people's top two worries.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Billionaire Stephen Smith is like the Magnus Carlsen of the mortgage business—at the top of his game and always thinking multiple moves ahead.

Starting from zero (he declared bankruptcy in 1984), Smith capitalized on various industry trends to methodically build a mortgage empire. Today, his holdings include stakes in

Billionaire Stephen Smith is like the Magnus Carlsen of the mortgage business—at the top of his game and always thinking multiple moves ahead.

Starting from zero (he declared bankruptcy in 1984), Smith capitalized on various industry trends to methodically build a mortgage empire. Today, his holdings include stakes in First National, Canada Guaranty, Home Trust, Equitable Bank, and Fairstone Financial.

We video-conferenced with Mr. Smith last week on a range of topics, including:

How tighter mortgage regulations helped make him rich(er)

How OSFI's loan-to-income (LTI) limit could change lending

How much additional mortgage regulation we need

Immigration's influence on housing

Whether Canada will ever see a liquid non-prime securitization market

What keeps him up at night.

So let's cut to the chase. In the exclusive video that follows, you'll get to know the humble grandmaster of Canadian mortgage entrepreneurship—possibly the most accomplished individual in our industry's history.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

💡April's Amortization Simulator update is now live, complete with the market's latest forward rate expectations. See Tools to download.

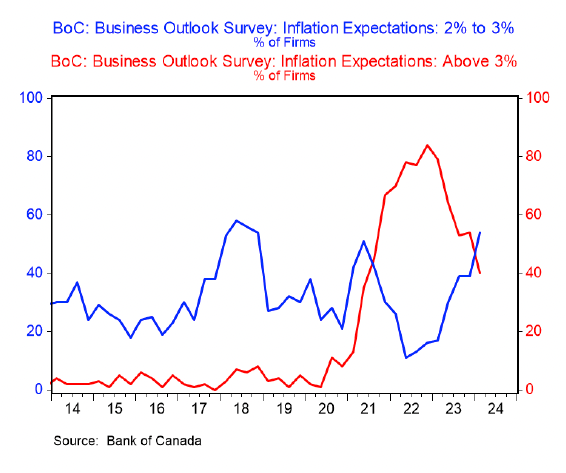

For the first time since 2021, the share of Canadian firms expecting year-ahead inflation over 3% is less than the percentage expecting 2-3%, reports BMO (chart below)

April's Amortization Simulator update is now live, complete with the market's latest forward rate expectations. See Tools to download.

For the first time since 2021, the share of Canadian firms expecting year-ahead inflation over 3% is less than the percentage expecting 2-3%, reports BMO (chart below). Raise a glass because that's a win.

Chart courtesy of BMO.

But wait, hold the champagne. Joe Canadian's wallet isn't feeling it. According to BoC data, consumers see no inflation progress for the next year.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

A gleaming luxury car in the driveway is a badge of honour for millions of Canadians. But for those on the hunt for home sweet home, flashier autos often equal humbler abodes.

Most Canadians innately understand the tradeoff. They get that a swanky, depreciating vehicle means a slimmer wallet come

A gleaming luxury car in the driveway is a badge of honour for millions of Canadians. But for those on the hunt for home sweet home, flashier autos often equal humbler abodes.

Most Canadians innately understand the tradeoff. They get that a swanky, depreciating vehicle means a slimmer wallet come retirement. Yet, they rationalize car splurges as an investment in happiness.

Happiness may be hard to quantify, but financial costs aren't. Sky-high car payments kill real estate dreams in more ways than one.

#1 — It's harder to save a down payment

Diverting another $600 monthly to a car means saving $32,512 less over 48 months—assuming a 6% tax-free return.

Stash that $600/month in a First Home Savings Account, and a middle-bracket earner could net another $8,000+ in tax breaks.

#2 — Buying power gets shaved

For an average Canadian family earning ~$140,000 last year, an extra $600/month car payment could spike their total debt service (TDS) ratios by over 5%-points.

That translates into almost $100,000 less buying power.

That's no small potatoes, given that 69% of homebuyers pay the maximum price they can afford, says CMHC.

#3 — Appreciation shrinks

Since 1981, the typical Canadian home has risen 5.78% over an average 12-month span.

Even if slower population growth and mounting supply result in just a 4% long-term appreciation rate, qualifying for $100,000 less house means a buyer forgoes:

$119,000 of tax-free gains after 20 years *

$167,000 of tax-free gains after 25 years *

$224,000 of tax-free gains after 30 years *

* Assuming it's a primary residence.

💡

4% appreciation would be 200 bps above inflation, assuming the Bank of Canada keeps hitting its 2% inflation target long-term. Nationwide home appreciation has averaged ~275 bps above inflation since 1981.

More car, less house

Let's zoom in on point #2 because it's the tradeoff between location, size, and home features that people feel the most.

Below are real examples of what buyers give up when they spend $600/month more on a car. We assume they've put 20% down, got a 30-year amortized mortgage at 4.99%, and have no other debt. Here's how upgrading their car downgrades their home options.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

If federally regulated mortgages were a club, OSFI would be the bouncer, and it's decided to be a bit more selective about who it lets in. The bank regulator's upcoming loan-to-income (LTI) limit will result in incrementally fewer borrowers being approved by prime lenders. That'

If federally regulated mortgages were a club, OSFI would be the bouncer, and it's decided to be a bit more selective about who it lets in. The bank regulator's upcoming loan-to-income (LTI) limit will result in incrementally fewer borrowers being approved by prime lenders. That's the bad news—if you're a prime lender or affected borrower.

The good news is that—apart from there being workarounds (more on that)—the calculation of LTI isn't as bad as some feared. Here's why, and note, we got these clarifications straight from OSFI:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Neo Financial wants to be your one-stop shop for financial services, and now it's rolling out the red carpet for mortgage brokers.

The company—known for its "Neo Money" and "Neo Credit" accounts, which dole out 5-15% cash back on purchases from Neo Partners—

Neo Financial wants to be your one-stop shop for financial services, and now it's rolling out the red carpet for mortgage brokers.

The company—known for its "Neo Money" and "Neo Credit" accounts, which dole out 5-15% cash back on purchases from Neo Partners—launched its mortgage lender in October. It gets its mortgage business mainly from cross-selling its credit card and investing customers. But as of this quarter, it has launched a pilot to drum up broker channel business.

The company launched in 2019, has big-time partnerships (e.g., Tim Hortons & Hudson's Bay) and counts over one million customers. It is backed by superstar venture capital investor Peter Thiel and has received $288M in funding to date.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

For a minority of mortgage shoppers, the price of leverage is going up.

Canada's banking watchdog, OSFI, has confirmed to MLN that it will enforce a new restriction on mortgage borrowing.

"The LTI measure we are implementing is a portfolio test that is designed to prevent the

For a minority of mortgage shoppers, the price of leverage is going up.

Canada's banking watchdog, OSFI, has confirmed to MLN that it will enforce a new restriction on mortgage borrowing.

"The LTI measure we are implementing is a portfolio test that is designed to prevent the buildup of highly leveraged loans during low interest rate periods," an OSFI official told MLN today.

Unlike the #stress test#, which is a borrower-specific limit, "the Loan to Income (LTI) measure is a portfolio test," the regulator says. Hence, there's no rule that says an individual borrower can't have an LTI over 4.5x. It's the lender that will determine what LTI they'll allow, subject to all other underwriting guidelines.

"This measure means that institutions, in any quarter, can only have a certain percentage of their mortgages in excess of 4.5x LTI," OSFI says. Previously, OSFI contemplated a 25% allowance above that threshold, but now it will be case-by-case, depending on the lender.

The new limit "applies to the institution’s portfolio of underwritten mortgages that originate that quarter and needs to be managed by the institution."

For borrowers, here's what this means in practical terms.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

📰Also in this edition:

• What the blockbuster immigration news means for real estate

• Mortgage Bytes

Well fancy this: a government watchdog is taking underdog borrowers under its wing.

In a submission today to the Department of Finance, Canada's Competition Bureau (CB) defended unfairly treated mortgage switchers, saying it

Also in this edition: • What the blockbuster immigration news means for real estate • Mortgage Bytes

Well fancy this: a government watchdog is taking underdog borrowers under its wing.

In a submission today to the Department of Finance, Canada's Competition Bureau (CB) defended unfairly treated mortgage switchers, saying it "urges policymakers to reconsider the application of the stress test at mortgage renewal for uninsured borrowers."

Doing so would "allow [borrowers] to switch lenders and benefit from competition," it explained.

What a concept. It kind of sounds like what the mortgage industry has been screaming from rooftops for 6+ years.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.