Fed chair Powell is like the James Bond of central banking – licensed to thrill.

And did he ever. The Fed banker with the golden gun started the rate festivities early this week, leaving mortgage originators feeling like they just hit the jackpot.

The 2-year #GoC# yield—which often front-runs BoC

Fed chair Powell is like the James Bond of central banking – licensed to thrill.

And did he ever. The Fed banker with the golden gun started the rate festivities early this week, leaving mortgage originators feeling like they just hit the jackpot.

The 2-year #GoC# yield—which often front-runs BoC policy changes—dove with U.S. rates. It's now below its 18-month moving average (MA) for the first time since 2021 (chart below).

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

📰Canadian 5-year yields hit half-year lows following Fed announcement.

It was a bombshell down in Washington D.C. today. The U.S. Federal Reserve has just signalled that liquidity will return to the mortgage market in 2024.

In a policy swivel that few saw coming, Fed chief Jerome Powell confirmed

Canadian 5-year yields hit half-year lows following Fed announcement.

It was a bombshell down in Washington D.C. today. The U.S. Federal Reserve has just signalled that liquidity will return to the mortgage market in 2024.

In a policy swivel that few saw coming, Fed chief Jerome Powell confirmed the Fed has already begun discussing when to "dial back" rate hikes—not that they will in the near future. To markets, that's the Fed effectively endorsing the peak rate thesis.

Canadian yields, moving in sympathy with Treasuries, plunged faster than Charlie Sheen's career after Two and a Half Men. The 5-year #GoC# is down 21 bps as we speak. We're hitting lows we haven't seen in half a year. On a point basis, today is the most significant drop since the March madness with U.S. banks.

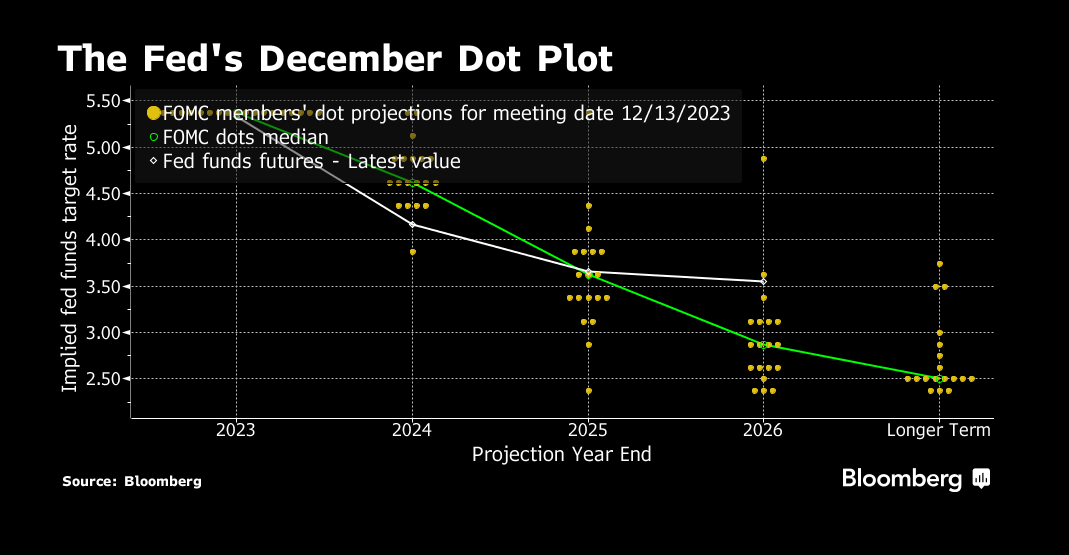

The New Crystal Ball: Rates Edition

Source: Bloomberg

Fed headliner Powell took to the stage in his presser and talked about "real progress in core inflation." As a result, #FOMC# members now see 75 bps in cuts in 2024 and more easing in 2025.

In Canada, market expectations are approaching five (5) rate cuts in 2024 (no joke), with the first in April. Here's the latest expected BoC rate path, as implied by Canada's #OIS# market.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

💡OSFI left its minimum qualifying rate (MQR) at 5.25% on Wednesday. Details below...

Trying to bring inflation back to 2% is starting to feel like trying to lose weight over the holidays—tough sledding.

Wednesday's U.S. CPI report was a reminder of that. Headline inflation ticked

OSFI left its minimum qualifying rate (MQR) at 5.25% on Wednesday. Details below...

Trying to bring inflation back to 2% is starting to feel like trying to lose weight over the holidays—tough sledding.

Wednesday's U.S. CPI report was a reminder of that. Headline inflation ticked down a notch to 3.1% from the previous 3.2%, moving with the urgency of a turtle herd. But core inflation seems to have attachment issues. It's been stuck in the 4.0 to 4.1% range for three months.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

For many in the business, 2023 was to the mortgage sector what pigeons are to statues.

Fortunately, the slate wipes clean in less than a month. With rate relief on the horizon and December volumes as slow as Toronto traffic, there's no better time to strategize on expanding

For many in the business, 2023 was to the mortgage sector what pigeons are to statues.

Fortunately, the slate wipes clean in less than a month. With rate relief on the horizon and December volumes as slow as Toronto traffic, there's no better time to strategize on expanding your presence, increasing efficiencies and fortifying your brand.

Here's a hit list of 25 tactics that might do just that. Not every tip will fit, but you'll probably find a couple to build your mortgage muscle in 2024.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

MIC investing is an effective way to generate yield while diversifying your portfolio from stocks, bonds and plain Jane real estate. But picking and choosing among MICs (mortgage investment corporations) isn't easy for a layperson. Most smaller investors must put all their MIC eggs in just one or

MIC investing is an effective way to generate yield while diversifying your portfolio from stocks, bonds and plain Jane real estate. But picking and choosing among MICs (mortgage investment corporations) isn't easy for a layperson. Most smaller investors must put all their MIC eggs in just one or two baskets.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

There's finally bustling rate activity in the mortgage market. It only took a 100 bps drop in yields to wake most banks up.

Let's talk uninsured mortgage rates to start. Leading nationally-advertised 5-year fixed rates are back below 6% for the first time in two months.

There's finally bustling rate activity in the mortgage market. It only took a 100 bps drop in yields to wake most banks up.

Let's talk uninsured mortgage rates to start. Leading nationally-advertised 5-year fixed rates are back below 6% for the first time in two months. HSBC is leading the charge with its 20 bps drop to 5.94%.

In the insured market, 5.19% is the new standard from national lenders, but why stop there? Regional discounter Butler Mortgage has already cracked the 5% barrier. Butler is now advertising a bought-down 5-year at 4.99%. Other cut-rate mortgage shops won't be far behind.

Meanwhile, at the Big 6, where rates fall slower than feathers in an updraft, our channel check confirms that median discretionary rates are on the downswing:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

The in-house lenders of major U.S. homebuilders are buying down mortgage rates like they're in a frenzy. It's become their go-to strategy to move new homes.

For example, America's largest homebuilder, D.R. Horton, offers rates a whopping 150 bps below the market.

The in-house lenders of major U.S. homebuilders are buying down mortgage rates like they're in a frenzy. It's become their go-to strategy to move new homes.

For example, America's largest homebuilder, D.R. Horton, offers rates a whopping 150 bps below the market. Smaller homebuilders with less assets and liquidity are like a mom-and-pop shop trying to price match with Walmart—they can't compete.

U.S. mortgage brokers and regular lenders can't compete either.

This isn't happening nearly as much in Canada. Take Mattamy, for example, North America's largest privately owned homebuilder. Its Canadian website features no mortgage discounts. Neither do the websites for a sampling of other top Canadian homebuilders we checked.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

In a world where cheering for unemployment feels as wrong as anchovies on pizza, history has a twisted way of saying, "You want lower rates? Well, it's gonna cost you - jobs!" And in today's episode of 'As the Economy Turns', we&

In a world where cheering for unemployment feels as wrong as anchovies on pizza, history has a twisted way of saying, "You want lower rates? Well, it's gonna cost you - jobs!" And in today's episode of 'As the Economy Turns', we've been handed yet another serving of that 'bad news casserole' we've developed a taste for.

Let's digest the mortgage consequences...

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Congrats to every financially stable borrower who got a 5-year fixed this month – you are philanthropists who generously donated to your lender's “We Love Your Money” foundation. And be sure to attend the next meeting of the "I Didn't Do the Math" club. It&

Congrats to every financially stable borrower who got a 5-year fixed this month – you are philanthropists who generously donated to your lender's “We Love Your Money” foundation. And be sure to attend the next meeting of the "I Didn't Do the Math" club. It's held regularly at the "Shoulda Got Better Advice" café.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

A Department of Finance official confirmed on Friday that the six Canadian Mortgage Charter (CMC) provisions are expectations (she called them "rules") but most won't be regulations.

The official wouldn't commit to saying banks had to follow all six rules, but they are "

A Department of Finance official confirmed on Friday that the six Canadian Mortgage Charter (CMC) provisions are expectations (she called them "rules") but most won't be regulations.

The official wouldn't commit to saying banks had to follow all six rules, but they are "expected" to.

"This is the government putting in black and white in a fiscal document what Canadians should expect when they are up for renewal," the official said, speaking on background. "And if they feel their banks are not holding up their end of the bargain, there are places they can turn to, like the FCAC."

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You hear it all the time, "Rental properties don't cash flow anymore," like it's some kind of universal truth.

But not every new rental is a money pit waiting to devour your wallet.

For property investors who like to skate to where the puck

You hear it all the time, "Rental properties don't cash flow anymore," like it's some kind of universal truth.

But not every new rental is a money pit waiting to devour your wallet.

For property investors who like to skate to where the puck is headed, it's about seeing opportunities where others see a closed door.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.