Banks across the land have been notifying customers of changes to their #readvanceable# mortgages.

Some of these notices appear written to create mass confusion. We've talked to a sampling of customers who got these letters and swore they were reading an alien dialect. Many are utterly bewildered by

Banks across the land have been notifying customers of changes to their #readvanceable# mortgages.

Some of these notices appear written to create mass confusion. We've talked to a sampling of customers who got these letters and swore they were reading an alien dialect. Many are utterly bewildered by what's happening—and why. (All of which makes a good touch point opportunity for mortgage advisors.)

The puzzlement stems from a policy change OSFI announced 15 months ago. Its new rules limit how customers with readvanceable mortgages can reborrow paid-down principal when the total borrowing is over 65% loan-to-value.

"OSFI expects that any and all lending above the 65% LTV limit, which cannot exceed 80% LTV, will be both amortizing and non-readvanceable," the regulator says.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

For weeks, we've been a Debbie Downer—warning that today's inflation report promised more frights than a Stephen King novel. And man, did StatsCan deliver a shocker.

Year-over-year inflation comparables and rocketing oil prices set us up for a doozy. But these numbers aren’t just

For weeks, we've been a Debbie Downer—warning that today's inflation report promised more frights than a Stephen King novel. And man, did StatsCan deliver a shocker.

Year-over-year inflation comparables and rocketing oil prices set us up for a doozy. But these numbers aren’t just bad; they're more like 'take your lunch money, give you a wedgie and swipe left on your Tinder profile' kind of bad.

Canada's not-so-hidden inflation dragon has re-emerged from its cave—breathing fire at 4%. Here are the sriracha-hot details:

Annual inflation: 4.0%, up from July's 3.3% (consensus: 3.8%)

Monthly inflation: Up 0.4% (consensus: 0.2%)

Average core inflation (y/y): 4.0% vs. 3.75% in July

Average core inflation (3-month): 4.5% vs. 3.5% in July

One key culprit this month was crude oil, which is high-stepping to a new 11-month high near $93/bbl. Technical analysis suggests potential continuation to at least $95+, barring contrary news.

Price of WTI Oil (Source: Refintiv EIkon)

Mortgage interest costs and rent were also a driver. But, that "is partly the lagged reaction to the Bank’s rate hikes in June and July, so shelter price growth will soon slow," says Capital Economics. In large part, the BoC is looking right through mortgage interest costs, a catalyst of their own doing.

What keeps the BoC most on the edge of their boardroom chairs are the core readings — especially the 3-month ones. And, "Previously, the Bank had been concerned that underlying trends looked like they were stuck around 3.5%," reported BMO Economics today. That view "now seems almost quaint."

Market reaction

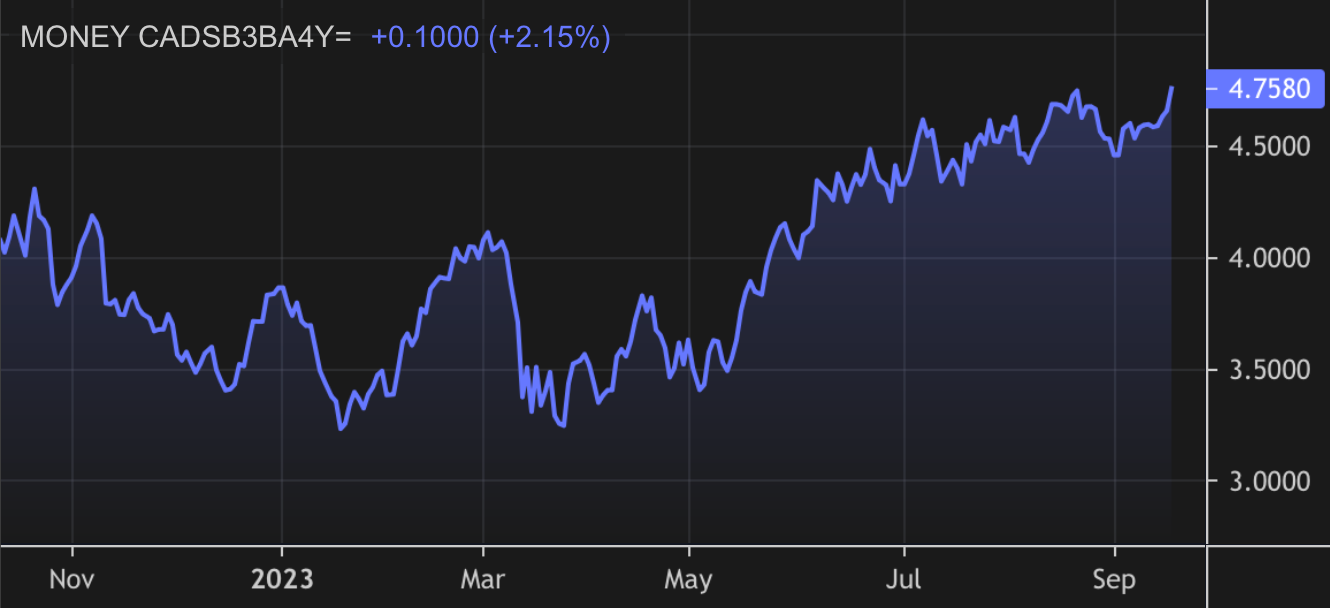

Canada's 4-year swap rate—a short-term leading indicator for fixed mortgage rates—is surging. It's up 10 bps as this is being written.

Chances of an October 25 BoC hike have doubled to 41%, with another hike now fully priced in by Q1 of 2024. But if we do get another 25 bps BoC bump, it'll likely be sooner.

Cuts are once again entirely off the board in the next 12 months—as this #OIS#-implied rate table below from Refinitiv Eikon illustrates.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

💡Reader note: This Week in RateLand will run Tuesday so it can reference Canada's latest inflation report.

OSFI's proposed "B-20" mortgage policy tightening will "push borrowers to commit mortgage fraud," expects a broker-lender CEO we spoke with off the record recently.

"

Reader note: This Week in RateLand will run Tuesday so it can reference Canada's latest inflation report.

OSFI's proposed "B-20" mortgage policy tightening will "push borrowers to commit mortgage fraud," expects a broker-lender CEO we spoke with off the record recently.

"We have seen a rise in fraudulent applications from borrowers frustrated with their continued inability to purchase a home," he said. "If OSFI wants to introduce more stress test type policies, they must simultaneously give federally-regulated financial institutions more abilities to fight mortgage fraud."

According to Equifax data cited by Cecely Roy at Mortgage Professionals Canada (MPC), mortgage fraud is already almost 30% higher than pre-pandemic. The only thing rising faster than that is the blood pressure of chief risk officers.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Sometimes a turtle in lead boots moves faster than our government. But hey, better late than never when it comes to this announcement.

The government has finally bent to pressure from housing groups and agreed to remove GST from purpose-built rental construction. Trudeau had sent that memo to his Finance

Sometimes a turtle in lead boots moves faster than our government. But hey, better late than never when it comes to this announcement.

The government has finally bent to pressure from housing groups and agreed to remove GST from purpose-built rental construction. Trudeau had sent that memo to his Finance Minister in 2015; really took the scenic route, didn't it?

This change gives rental construction a big shot in the arm. It also gives financing pros a shiny new reason to polish their PowerPoint slides and dial up their 4-plus-unit builder contacts.

We asked Canadian Home Builders' Association (CHBA) CEO Kevin Lee to break it down.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

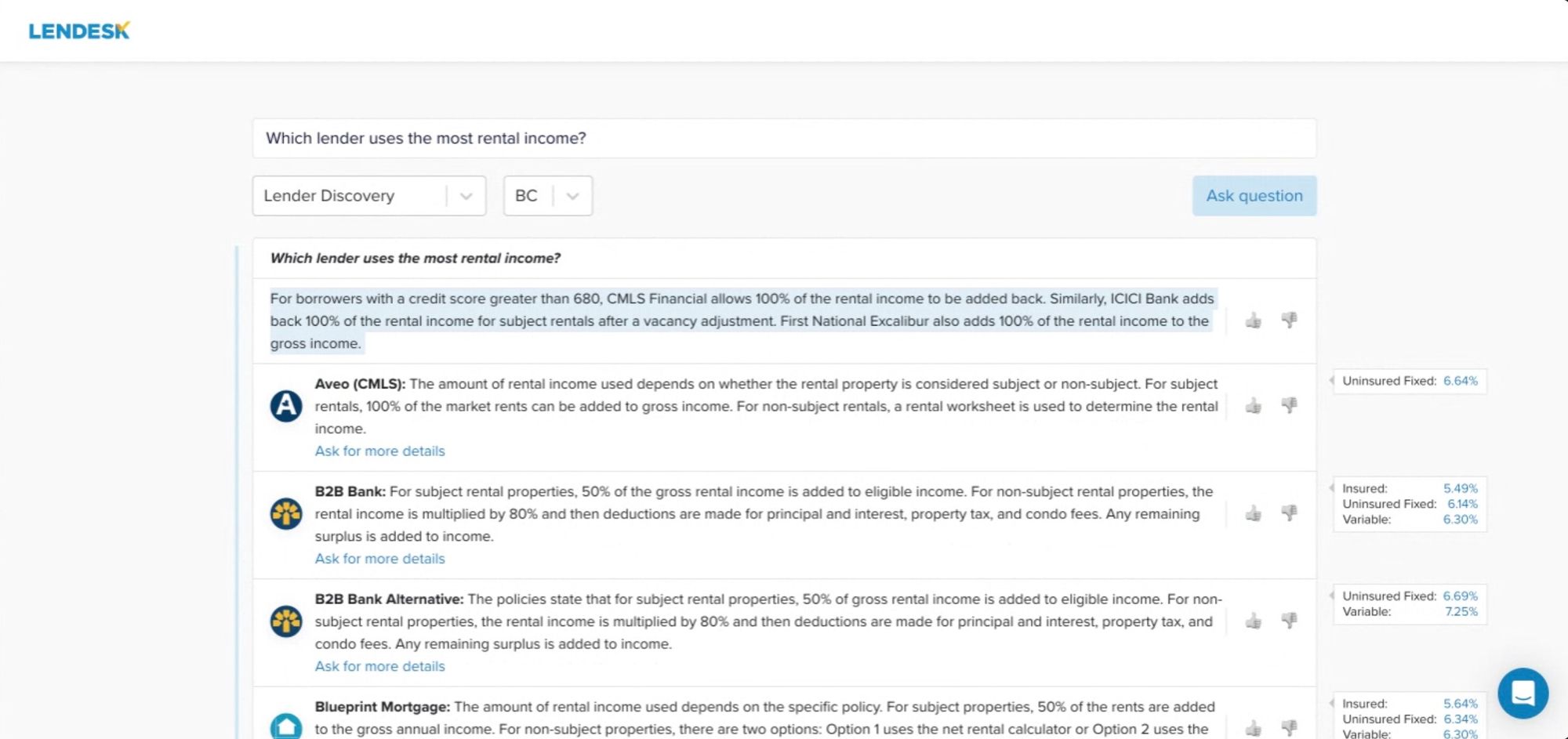

Artificial intelligence (AI) is destined to penetrate every nook and cranny of the mortgage business. That's why, in the days and months to come, we'll profile a parade of AI tools to help borrowers and mortgage advisors. And we'll start with this one.

It&

Artificial intelligence (AI) is destined to penetrate every nook and cranny of the mortgage business. That's why, in the days and months to come, we'll profile a parade of AI tools to help borrowers and mortgage advisors. And we'll start with this one.

It's called Lender Spotlight AI Assistant, and it's from Lendesk.

Like a digital bloodhound, AI Assistant sniffs through a whopping 7000+ lender policies, figuring out which lender might consider a given mortgage scenario.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

"...It would be a very brave central bank indeed to be even considering hiking rates with the latest quarterly GDP report printing negative."

—BMO Economics

That's the orthodox playbook, anyway.

But the Bank of Canada could unexpectedly take the road less travelled, kind of like the

"...It would be a very brave central bank indeed to be even considering hiking rates with the latest quarterly GDP report printing negative." —BMO Economics

That's the orthodox playbook, anyway.

But the Bank of Canada could unexpectedly take the road less travelled, kind of like the Detroit Lions faking a punt inside their 20-yard line on Thursday, with 27 million fans watching.

The BoC may need a surprise play of its own because we're by no means out of the woods on inflation. It knows that rising price levels and a slowing economy can co-exist despite last quarter's negative GDP print. We've seen that odd couple before, back in the disco era of '76 to '82.

The BoC would rather play the Grinch who stole borrowers' paychecks than be accused of letting the inflation horse back out of the barn. That's why its communications have left the door open for an insurance hike, even amidst a waning economy.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Getting inflation down is like wrestling a greased pig. Sometimes, it gets away from you for a while.

This fall will be one of those times.

Getting headline inflation back in the twos won't come easy. If you want to understand how challenging the Bank of Canada'

Getting inflation down is like wrestling a greased pig. Sometimes, it gets away from you for a while.

This fall will be one of those times.

Getting headline inflation back in the twos won't come easy. If you want to understand how challenging the Bank of Canada's task is, consider the following.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

The Manulife One (M1) has always been one of the most powerful and flexible products in the mortgage market. But as slick as it is, the broker version was like a Brioni suit with a mustard stain—somewhat flawed.

But now, Manulife has ironed out a few of the wrinkles.

The Manulife One (M1) has always been one of the most powerful and flexible products in the mortgage market. But as slick as it is, the broker version was like a Brioni suit with a mustard stain—somewhat flawed.

But now, Manulife has ironed out a few of the wrinkles. So, let's review this mini-M1 makeover and see what they've done.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Canada would be better off if pesky variable-rate mortgages with fixed payments were "less prevalent," says our banking regulator.

Oftentimes, when rates surge, their "fixed payments do not cover the interest payments and mortgage principal outstanding grows," said Superintendent Peter Routledge in a keynote speech at

Canada would be better off if pesky variable-rate mortgages with fixed payments were "less prevalent," says our banking regulator.

Oftentimes, when rates surge, their "fixed payments do not cover the interest payments and mortgage principal outstanding grows," said Superintendent Peter Routledge in a keynote speech at Thursday's Scotiabank Financials Summit.

"In fact, the contractual amortization period does not change. And mortgagors will have to make up the deferred principal paydowns when they renew. This means they are at risk of suffering a significant payment shock."

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

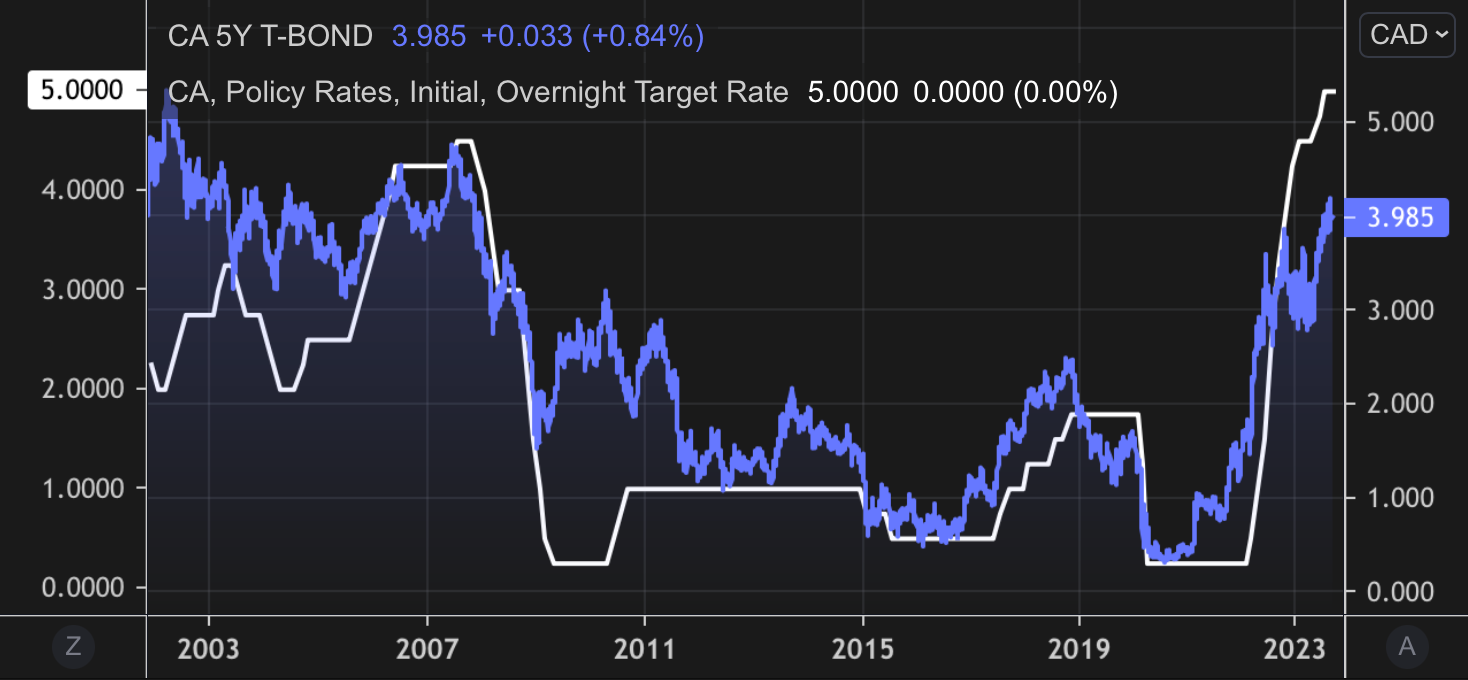

The Bank of Canada, widely known for its plot-twist-worthy decisions, went for the predictable ending this round. It left its key policy rate at a 22-year high of 5.00% - just as the bond market expected.

Compared to a 25 bps hike, today's rate pause saved an

The Bank of Canada, widely known for its plot-twist-worthy decisions, went for the predictable ending this round. It left its key policy rate at a 22-year high of 5.00% - just as the bond market expected.

Canada's overnight rate versus 5-year bond yield (Source: Refinitiv)

Compared to a 25 bps hike, today's rate pause saved an average floating-rate borrower from seeing up to a $70 increase in their monthly payment. (The average Canadian mortgage amount is $351,692, according to the latest TransUnion data.)

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.