Some lenders have an unconventional idea of partnership. They boldly label brokers as their "partners" but treat them with the same respect one might reserve for a telemarketer who calls during dinner.

If you're a lender, one strange way to show broker partners you 'care&

Some lenders have an unconventional idea of partnership. They boldly label brokers as their "partners" but treat them with the same respect one might reserve for a telemarketer who calls during dinner.

If you're a lender, one strange way to show broker partners you 'care' is to withhold your best rates from them, giving the lowest pricing only to your retail reps. It's almost like telling brokers, "You're expendable. Deal with it."

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

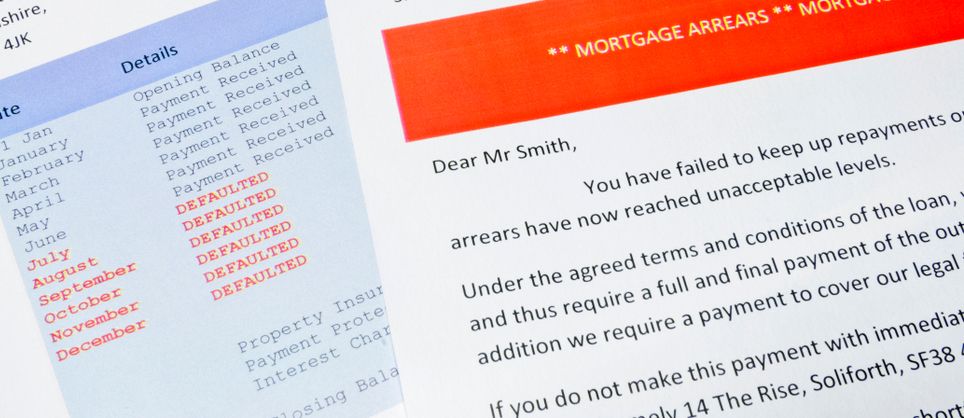

Eighteen months into one of the most vigorous hiking cycles in history, 90-day #prime mortgage# arrears are still dragging along the historical bottom at just 15 bps. A year ago, virtually every analyst in the game thought they'd be higher by now.

But the fact that 90-day arrears

Eighteen months into one of the most vigorous hiking cycles in history, 90-day #prime mortgage# arrears are still dragging along the historical bottom at just 15 bps. A year ago, virtually every analyst in the game thought they'd be higher by now.

But the fact that 90-day arrears are less than half the 36 bps long-term average is no longer a mystery. Low unemployment, strong equity positions, government intervention, supportive banks, accumulated savings, strong underwriting and other factors are keeping Canadians in their homes and jingle-mail at bay.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

The world's most influential bond, America's 10-year Treasury, is making a brisk run for its 4.34% October high (chart above). That's raising the stakes for beleaguered borrowers on both sides of the border.

This latest yield sprint comes on the heels of:

The world's most influential bond, America's 10-year Treasury, is making a brisk run for its 4.34% October high (chart above). That's raising the stakes for beleaguered borrowers on both sides of the border.

This latest yield sprint comes on the heels of:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Regardless of your political leanings or stance on the ever-delicate immigration and housing debate, it's hard not to have a soft spot for Canada's new Housing Minister, Sean Fraser. Ambitious, affable, and apparently not just in it for the office decor, he sat down with us

Regardless of your political leanings or stance on the ever-delicate immigration and housing debate, it's hard not to have a soft spot for Canada's new Housing Minister, Sean Fraser. Ambitious, affable, and apparently not just in it for the office decor, he sat down with us on Monday.

The agenda? A trifecta of probing questions, including:

Will Canada put the brakes on immigration, or is housing construction in a perpetual game of catch-up?

Is the government merely wringing its hands over middle-class homebuyers, or is there a plan in the works to help them?

Just how deep are taxpayers' pockets when it comes to "solving" the housing crisis?

For those seeking answers straight from the Minister's mouth, check out MLN's exclusive video interview that follows.

0:00

/15:59

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

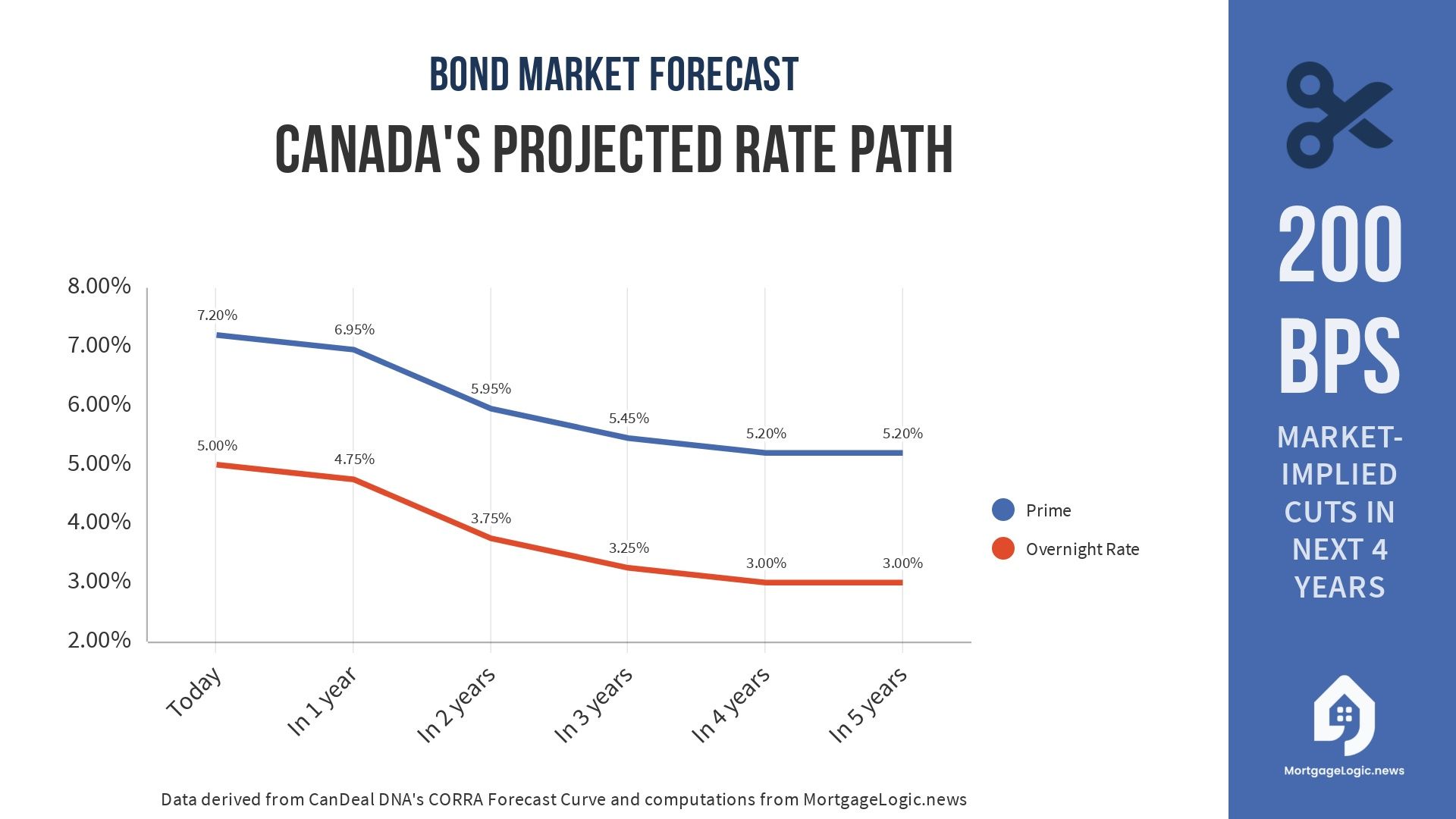

Interest rate commentators have long relied on overnight index swaps (#OIS#) and forward markets to crystal ball rate direction. Now, with CORRA elbowing CDOR aside as Canada's financial benchmark rate, some of those forecasting tools are going the way of the floppy disk.

That's led MLN

Interest rate commentators have long relied on overnight index swaps (#OIS#) and forward markets to crystal ball rate direction. Now, with CORRA elbowing CDOR aside as Canada's financial benchmark rate, some of those forecasting tools are going the way of the floppy disk.

That's led MLN on a hunt for a more effective rate indicator, and we recently found one in the brand new CORRA forecast curve.

Published exclusively by CanDeal DNA, the leading provider of valuations for Canada's fixed-income market, the CORRA forecast curve reflects bets from institutional traders on where the Bank of Canada will take its key lending rate over the next five years. It'll be the basis for MortgageLogic.news' weekly long-range outlooks, as well as the default rates in MLN's exclusive amortization simulator.

Despite the massive variability in any market rate forecast beyond 6-12 months, this new tool should improve forecast accuracy and get better over time (as liquidity builds in its underlying derivatives).

For MLN subscribers, it's a secret sauce for cooking up more realistic hypothetical mortgage scenarios, without the usual dash of wishful thinking.

💡

Pro Tip: Borrowers should understand (and be told) that market-implied rate forecasts are helpful only as a baseline possibility for what might transpire with rates—based on the market's best current analysis of macroeconomic factors. Scenario planning should therefore include "best and worst" scenarios (e.g., by adding/subtracting 100 to 200 bps to market rate forecasts, assuming higher rates for longer/shorter, etc.).

Here's why the CORRA forecast is a step up from prior projection tools and what it's forecasting now.

Why the CORRA forecast curve

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

As pundits debate whether the economy will glide in like a feather on a gentle breeze or plummet like Canadians' savings balances, Moody's threw markets a curveball Tuesday.

The ratings agency downgraded a slew of U.S. mid-size banks. Its reasons included rising funding costs, tightened lending,

As pundits debate whether the economy will glide in like a feather on a gentle breeze or plummet like Canadians' savings balances, Moody's threw markets a curveball Tuesday.

The ratings agency downgraded a slew of U.S. mid-size banks. Its reasons included rising funding costs, tightened lending, declining earnings, interest rate risk, potential regulatory capital constraints, commercial real estate exposure, collateral risk, and deposit risk—take your pick.

This is the latest misfortune for non-money center banks, who've taken it on the chin. But what does this financial wrinkle have to do with Canadian mortgage rates?

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Rental and commercial boutique lender Glasslake Funding just made a push into Alberta and B.C. We caught up with Glasslake President and former Home Trust Underwriting EVP Mike Forshee to check on the opportunities he's prospecting out there.

He tells us, "We will continue to go

Rental and commercial boutique lender Glasslake Funding just made a push into Alberta and B.C. We caught up with Glasslake President and former Home Trust Underwriting EVP Mike Forshee to check on the opportunities he's prospecting out there.

He tells us, "We will continue to go into secondary markets in the western provinces" for one simple reason. The risk profile in B.C. and Alberta are "very similar" to Ontario, where Glasslake is based.

One offering he sees consistent demand for is AirBNB financing. "We are seeing a real opportunity in Alberta for this product," Forshee says. "Given the values in Alberta are lower than in the GTA and Vancouver..."

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

It was a double-header for jobs numbers Friday, and the bond market was on the edge of its seat, hoping for signs of a downshifting economy.

What we got were two semi-promising reports but with more gaps than a teenager's text message.

Of course, the compass for rate

It was a double-header for jobs numbers Friday, and the bond market was on the edge of its seat, hoping for signs of a downshifting economy.

What we got were two semi-promising reports but with more gaps than a teenager's text message.

Of course, the compass for rate direction depends on how traders interpret the data's mixed messages. So, grab some crackers and let's dig into it...

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

First National, a top 5 player in the broker market, recently put a new spin on its rental property underwriting guidelines, adding a touch more flexibility.

In a time when so many investors have gone into hibernation, however, the move may seem curious to some. Intrigued by this shift, we

First National, a top 5 player in the broker market, recently put a new spin on its rental property underwriting guidelines, adding a touch more flexibility.

In a time when so many investors have gone into hibernation, however, the move may seem curious to some. Intrigued by this shift, we connected with First National's Senior Vice President, Scott McKenzie, to understand the logic behind the change.

Here's how he explained it.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

BMO's highly anticipated re-entry into the broker market is more than just a headline – it's a robust "vote of confidence in the broker channel" declared BMO Capital Markets analyst Étienne Ricard today.

On First National's conference call today, Ricard questioned CEO Jason

BMO's highly anticipated re-entry into the broker market is more than just a headline – it's a robust "vote of confidence in the broker channel" declared BMO Capital Markets analyst Étienne Ricard today.

On First National's conference call today, Ricard questioned CEO Jason Ellis about it, asking, "What do the banks value most in the broker channel that is more challenging to replicate in more traditional distribution channels?"

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.