Canada would be better off if pesky variable-rate mortgages with fixed payments were "less prevalent," says our banking regulator.

Oftentimes, when rates surge, their "fixed payments do not cover the interest payments and mortgage principal outstanding grows," said Superintendent Peter Routledge in a keynote speech at Thursday's Scotiabank Financials Summit.

"In fact, the contractual amortization period does not change. And mortgagors will have to make up the deferred principal paydowns when...

MLN NewsStream

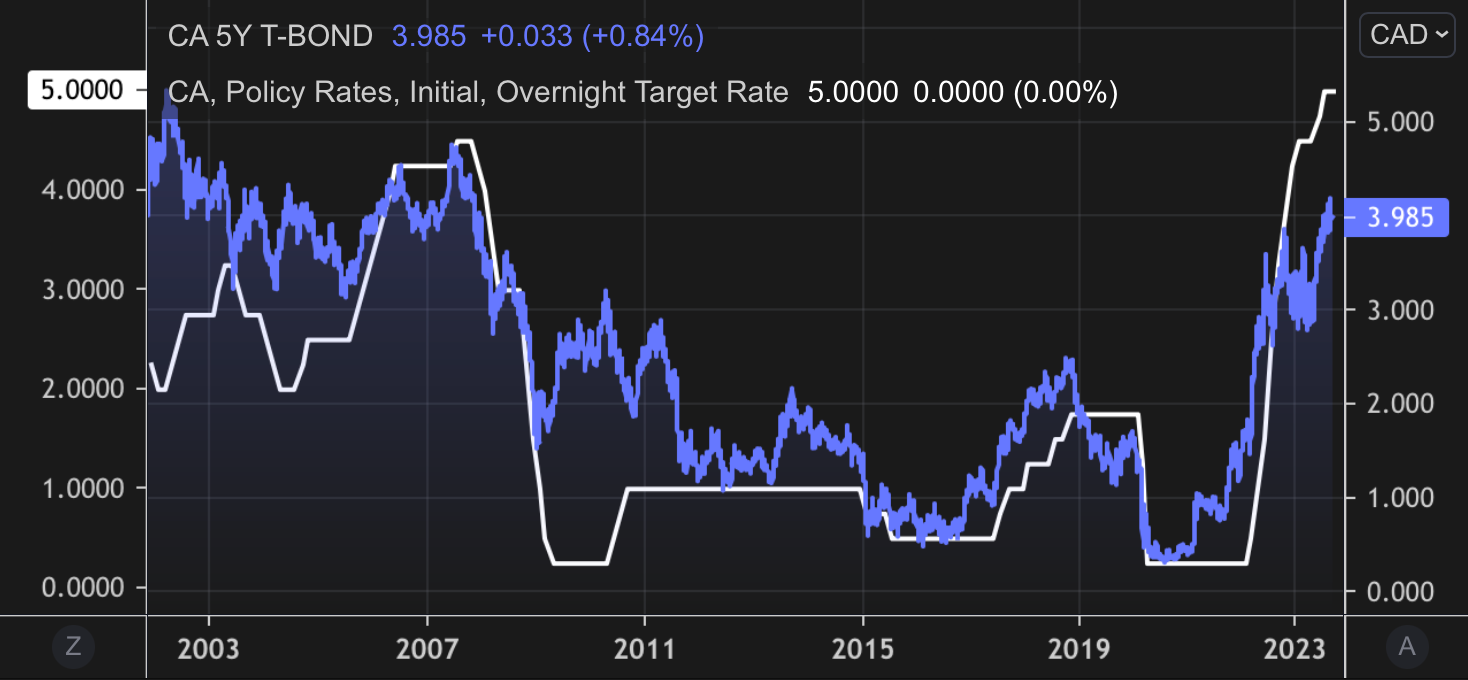

Bank of Canada Suspends Rate Hikes Again

The Bank of Canada, widely known for its plot-twist-worthy decisions, went for the predictable ending this round. It left its key policy rate at a 22-year high of 5.00% - just as the bond market expected.

Compared to a 25 bps hike, today's rate pause saved an average floating-rate borrower from seeing up to a $70 increase in their monthly payment. (The average Canadian mortgage amount is $351,692, according to the latest TransUnion data.)...

WealthOne Bank: Will the Regulatory Whirlwind Blow Away?

WealthOne Bank of Canada is one of the most competitive near-prime lenders. So, it was concerning to hear that it's under Finance Minister Chrystia Freeland's microscope.

Her scrutiny of the company was reported by the Globe this weekend. In a nutshell, the DoF made the company jump through all sorts of hoops due to alleged concerns about national security and potential money laundering. Among other things, Freeland's office forced the bank to cut ties with three key investors with apparent li...

Pine Goes National Next Week (sans Quebec)

It's always interesting to check in with mortgage fintechs like Pine. After all, if investors like Greylock Partners, Inovia Capital and Intact Ventures value the company at $75 million and hand them $30 million, they must be doing something unique.

On Sept. 11, Pine unfurls itself nationally across Canada—everywhere but Quebec (possibly because of the nightmarish red-tape, language rules and compliance environment in the province).

The company sells an ultra-low rate and targets a younger d...

Cloudy with a Chance of Recession. New Data Alter the Rate Forecast

Canada's economy needs stormy weather before the sun can shine. And on Friday, we got some dark clouds.

Our economy shrunk, and joblessness surged below the border. For all anyone knows, Canada may already be in the midst of a technical recession (defined as two consecutive quarters of negative growth).

For low-rate enthusiasts, it was a glimmer of hope that the top in rates might be in. Canada's 4-year swap rate dove another 7 bps, per the chart above. And—while it's not unheard of that som...