Washington's political establishment is nearing a resolution on the debt ceiling fiasco. With a bit of last-minute horse-trading, Congress should be able to lift the debt limit by the Treasury Department's revised June 5 deadline.

That should hopefully remove some upward pressure on U.S. yields, which have combined with CPI concerns to take Canadian fixed rates higher.

"The bulk of the recent back-up in Treasury yields has been in real yields, not in the implied inflation premium," BMO said Fr...

MLN NewsStream

1-on-1 with Stephen Poloz: Part II

"Do you really want to make a big bet that you do know what's going on right now?"—Stephen Poloz on mortgage term selection

In this much-anticipated follow-up with our prior BoC Governor, Stephen Poloz, he saves the best for last. Students of monetary policy, mortgage strategy and housing dynamics should find it well worth the 30 minutes.

Among the topics Mr. Poloz covers:

* The substantial weight the BoC puts on the U.S. outlook when setting policy

* How, and how often, the BoC and Fed com...

Mortgage notables from RBC's, TD's & CIBC's Q2 reports

Anecdotes from our megabanks lend a sense for what's happening throughout the prime mortgage market. That's why we pour through their quarterlies (every quarter).

Among the general trends they reported in the second quarter:...

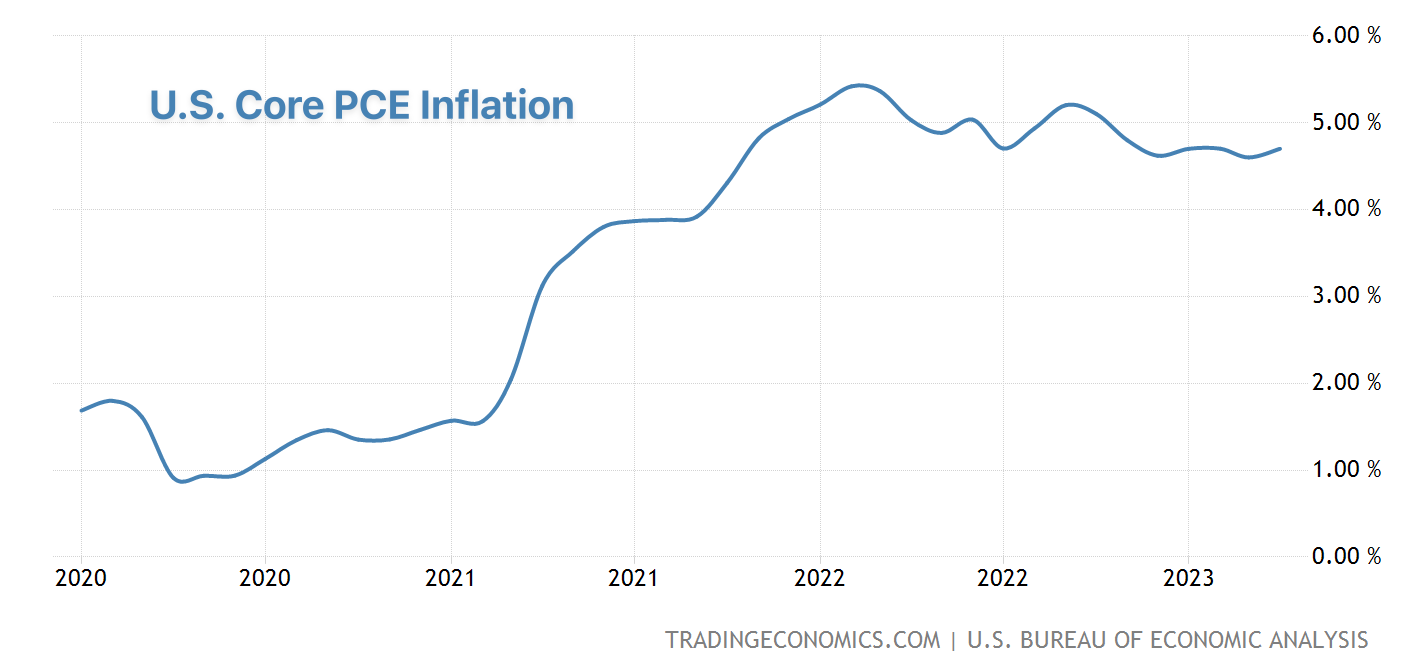

Hot PCE pushes implied rate hike expectations to 100%

The Fed's go-to inflation indicator has exceeded expectations again.

The so-called "core PCE deflator," which excludes food and energy, landed 0.1% above consensus, rising 0.4% m/m and 4.7% y/y in April. That's up from 0.3% m/m and 4.6% y/y in March.

Services inflation was even worse, leaping 5.5% y/y compared to 4.6% previously.

Inflation is not only hanging around, it's going in the wrong direction. As far as central bankers are concerned, there are still too many people with jobs, buying t...

This & That: The U.S. risks a downgrade

...